》Check SMM lead product quotes, data, and market analysis

》Subscribe to view historical spot prices of SMM metals

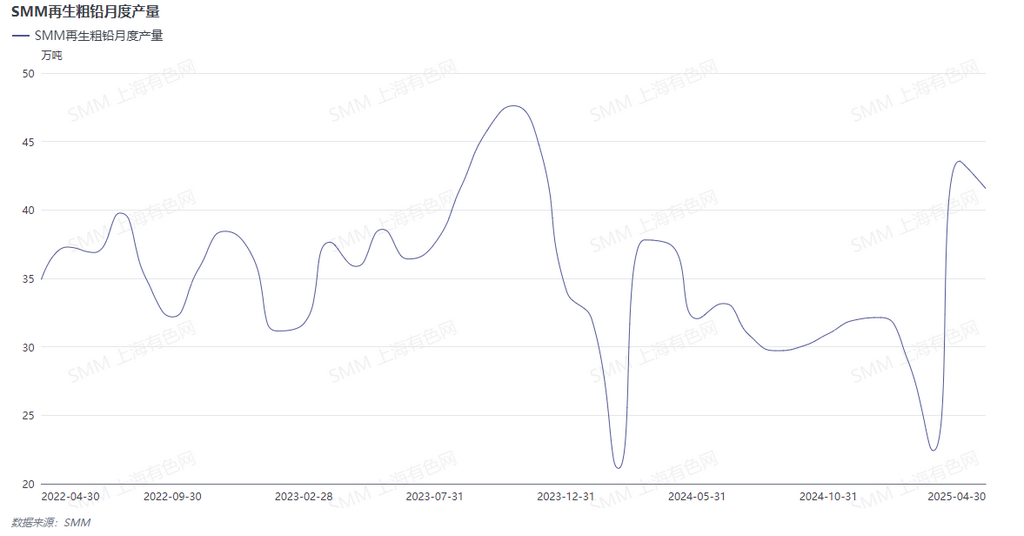

>SMM April 30 Report:

>In April 2025, the production of secondary crude lead declined, decreasing by 4.56% MoM and increasing by 11.04% YoY. The production of secondary refined lead also decreased by 4.26% MoM, while increasing by 7.46% YoY.

>In March, the price center of lead ran relatively high, and secondary lead smelters achieved good profitability, leading to high production enthusiasm. Coupled with the launch of large-scale new capacity, production resumptions and ramp-ups at large and medium-sized smelters, the production of secondary lead in March reached a new high in the past 1.5 years. April is the traditional consumption off-season for lead-acid batteries, with weak willingness from downstream battery producers to purchase lead ingots. Additionally, the low scrap volume in the scrap battery market, combined with the high operating rate of secondary lead production, exacerbated the sentiment of recyclers to hold back cargoes. Tight raw material supply, high costs, and low selling prices of finished products led to significant operational pressure on secondary lead smelters, resulting in widespread production cuts and suspensions at month-end. Therefore, production in April declined significantly compared to March.

>In May, downstream battery producers generally have plans for holiday shutdowns during the Labor Day holiday, with weak demand for lead ingot purchases. Most secondary lead smelters that have reduced or suspended production have indicated that they need to observe market conditions in May before deciding whether to resume normal production. SMM expects that the production of secondary lead in May may remain stable or decline slightly.